Opinion Leaders

Opinion Leaders

An important look at high-frequency data for investors

-

Eurizon

In recent weeks, the global macroeconomic environment has been characterised by a dramatic rise in uncertainty.

This is linked to the unpredictability of developments in the conflict that the US and Israel initiated against Iran on 28 February. To assess the initial impact of this crisis on national economies, it can be helpful to look at so-called high-frequency data. This data is published daily or weekly and provides timely insights into economic developments.

US economy

For the US economy, the Weekly Economic Index published by the Federal Reserve Bank of Dallas provided signs of a significant upturn. In the week ending 11 April, the indicator’s estimate was consistent with real GDP growth of 2.8% year-on-year. This represents a slight increase from the previous figure of 2.69%. With regard to employment, growing uncertainty is leading companies to rely increasingly on temporary staff. Since the start of the year, the ASA Staffing Index, a weekly indicator of trends in the filling of temporary and fixed-term positions in the US, has shown a gradual rise. In the week ending 5 April, it stood 4.8% above the 2025 level. With regard to consumption in the US, the Federal Reserve Bank of Chicago’s real-time estimates (CARTS Nowcast) for March show a nominal increase in retail sales excluding cars of 1.3% compared with the previous month. However, on an inflation-adjusted basis, sales fell by 0.7% in real terms compared with the previous month. This estimate suggests that the loss of consumer purchasing power resulting from the recent sharp rise in consumer prices, particularly in the energy sector, is likely to have dampened real consumption.

Furthermore, the Federal Reserve Bank of Cleveland’s nowcasting models for US consumer price inflation point to a further rise in April, following a significant increase in March. For April, the Cleveland Fed estimates that the headline inflation rate will rise to 3.58% year-on-year, up from 3.3% in March. This corresponds to a month-on-month increase of 0.46%. The core rate, by contrast, is expected to stabilise largely at 2.6% year-on-year, with a month-on-month increase of 0.21%.

German economy

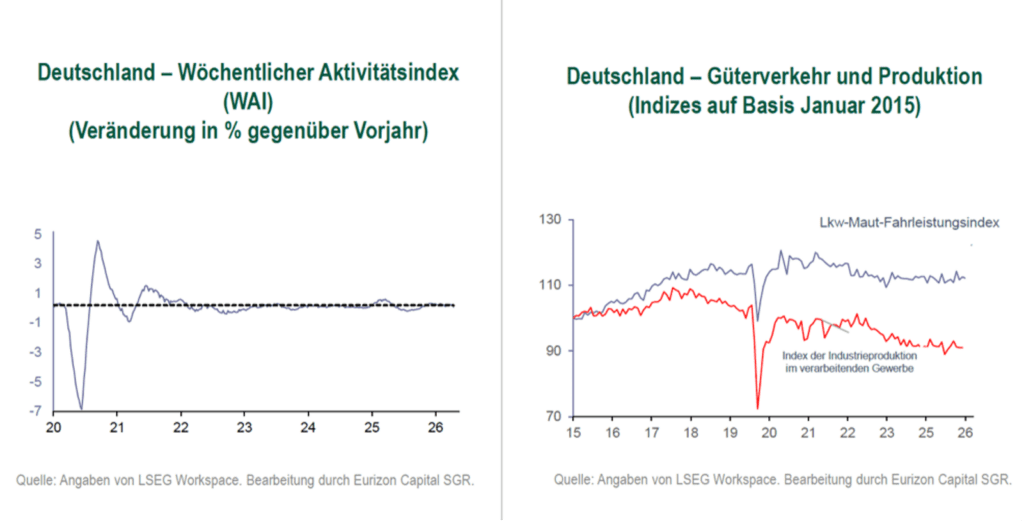

As regards the German economy, the Weekly Activity Index (WAI) compiled by the Deutsche Bundesbank on the basis of an analysis of both monthly and higher-frequency data on a weekly and daily basis recorded a value of minus 0.12 in the 17th week of 2026, the week ending 24 April. This represents a slight slowdown compared with the figure of 0.01 in the previous week. The average value for the weeks available since the start of the year stands at 0.02, reflecting a subdued trend in German economic activity in the first half of the year.

In relation to the trend in industrial activity, the index of kilometres travelled by toll-paying lorries on German motorways, published by the Federal Statistical Office (Destatis) – a figure that tends to correlate with industrial production – recorded a 0.3% decline in March compared with the previous month. In February, it had risen by 0.7% compared with the previous month. Although the trend in this indicator remains quite volatile, its performance in the first quarter of the year as a whole points to only a limited recovery in the German industrial economy.

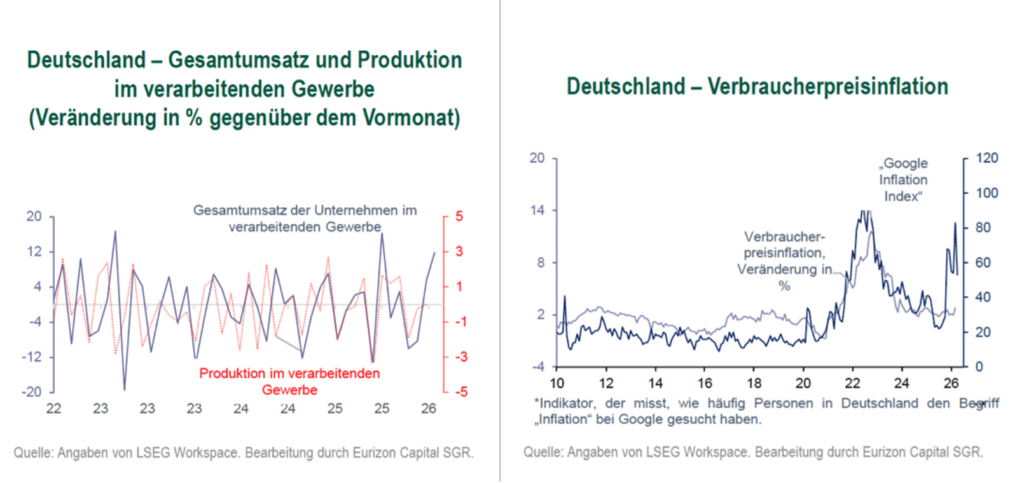

By contrast, the preliminary estimate of the indicator for total turnover in the manufacturing sector, compiled by the Federal Statistical Office (Destatis) as part of its experimental statistics, provided indications of a more pronounced recovery in production in the German manufacturing sector in April. According to the preliminary estimate, total turnover in the manufacturing sector rose by 11.8% in March compared with the previous month, following a 5.6% increase in February. The data are not seasonally adjusted. These estimates point to a more pronounced recovery in manufacturing activity in April.

As regards price trends in Germany, the “Google Inflation Index” – an indicator that tracks the number of daily Google searches in Germany for the term “ ” and is generally correlated with inflation trends – points to a sharp rise in concerns about price trends in March, which only partially eased in April. The recent rise in inflation, combined with fears of future price increases, could slow down consumption growth if it persists.