Focus

Focus

China: a country in a technological frenzy

-

Wolfgang Hagl

Redaktor

One of the distinctive features of the Chinese model of success is that it has emerged from a peculiar symbiosis of a capitalist market economy and a socialist planned economy. The Five-Year Plans are among the key policy instruments used by the political leadership in Beijing. These set out the economic, technological, and social objectives for the next five years. The most recent document of this kind was adopted by the National People’s Congress at the beginning of March. The 141-page work-ing paper, which is also being studied with great interest abroad, is regarded as one of the most important of its kind in a long time. With the 15th Five-Year Plan, the Asian superpower aims to take the next step in its evolution and become an autonomous technological nation.

What are Beijing’s objectives?

According to the Five-Year Plan, the digital economy’s share of China’s gross domestic product (GDP) is set to rise to 12.5% by 2030. At first glance, this may not seem like a big deal. However, a comparison with Western countries reveals the true significance of this figure. In Germany, for example, Europe’s largest economy, the digital economy accounts for only around 4.5% of GDP. Another of Beijing’s goals is to increase investment in research and development by more than 7% per year. Furthermore, the number of high-quality patents is set to rise from 16 to 22 per 10,000 inhabitants. By way of comparison, this figure stands at 11.4 in Switzerland.

Where China is already leading the way

One area of technology in which the country has already achieved a leading position is robotics. Humanoid robots are considered a major market of the future in this field. According to a study by the British bank Barclays, the People’s Republic holds the technological lead in the mass production and development of these intelligent machines. China is also at the forefront globally when it comes to 5G mobile communications standards, solar panel production, electric mobility, and lithium-ion battery production. In the high-tech fields of artificial intelligence, cloud computing, big data and quantum computing, the US is currently still ahead, but its lead is dwindling.

Competitive advantage through rare earths

China has set itself the goal of achieving technological independence. This means that the entire value chain is to be covered within its own borders. The country does not wish to be reliant on foreign materials, intermediate products or expertise. China’s advantage: with a global market share of 60% to 70%, the country is the largest producer of rare earths. China not only possesses enormous reserves, but also a well-developed infrastructure for the further processing of these scarce raw materials. Rare earths are a group of elements found in many high-tech products. Among other things, they are indispensable for the manufacture of smartphones, computers, flat-screen displays and LEDs. Furthermore, they also play an important role in electric motors, wind turbines, medical technology and the aerospace industry.

It’s not all rosy

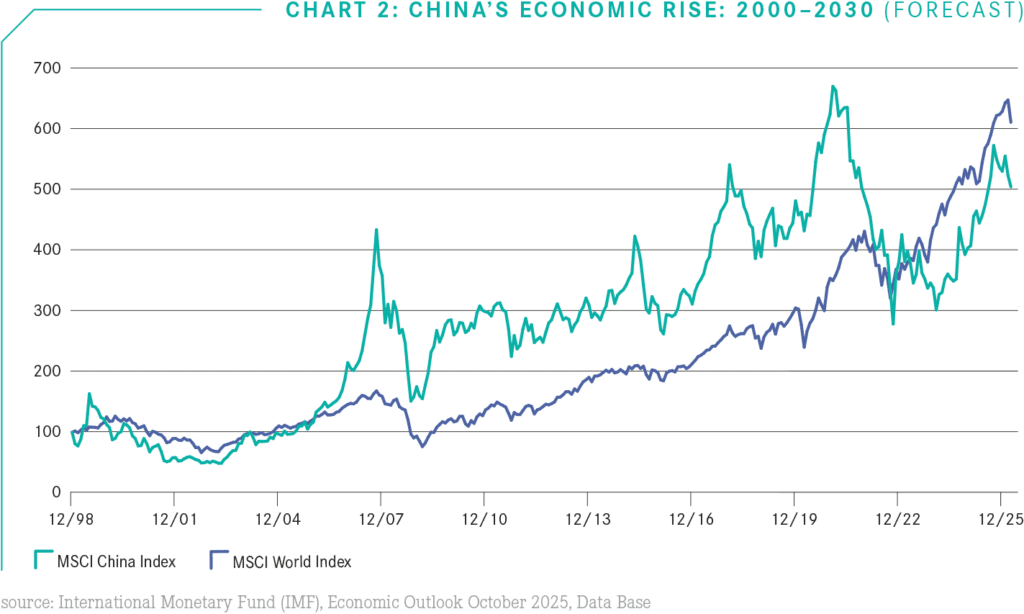

China not only has the prerequisites in place, but also the will and the resources to establish itself as a technology powerhouse driven by innovation. Investments in selected sectors such as robotics or the digital economy are, therefore, particularly attractive. More on that later. First, however, let’s take a look at the latest developments. As chart 3 demonstrates, the Chinese stock market (as measured by the MSCI China Index) has still not fully recovered from its crash in spring 2020 caused by the Covid pandemic. So what has been holding China back?

China’s ailing old economy

China’s growth model, which has achieved such impressive growth in the past, has been facing significant headwinds for some time now. The ongoing consolidation in the property sector and its impact on local government finances have led to a persistent weakness in domestic demand and deflationary pressures. Weak domestic consumption has, at least, been compensated by strong export growth, which has been partly supported by a depreciation of the real exchange rate. However, heightened global trade tensions make reliance on exports less sustainable for maintaining robust growth in the future. Beijing has, therefore, been wise to dampen the euphoria surrounding the growth target for 2026. GDP is expected to rise by between 4.5% and 5.0%, with the lower end of the range representing the lowest growth target since 1991. This means the government will not have to launch new support programmes immediately should the economy veer off course.

Chinese investments which make sense

In the short term, the Chinese economy remains vulnerable to disruptions. Given the current consumer sentiment, it is uncertain whether domestic demand will regain momentum. Meanwhile, new trade conflicts are a sword of Damocles over exports. Added to this are uncertainties regarding the impact of the Iran war on energy prices and the global economy. Investors should brace themselves for a period of higher volatility when investing in China and, if in doubt, avoid cyclical sectors. For those who look beyond their own nose and think in longer terms, investments focusing on the Chinese technology sector could be worthwhile. There is a whole range of investment opportunities in this area.

Disruptive forces as an investment opportunity

The first recommendation is for a Vontobel Tracker Certificate maturing in February 2026 that tracks the Rising Economies Disruptors Index (ZRISCV). Specifically, the strategy invests in up to 50 shares of companies which, in the view of the index sponsor Vontobel Asset Management, are set to benefit from technological progress and the associated upheavals in China and other Asian countries. The focus is on companies that drive innovation, offer disruptive products or utilise disruptive technologies in their business models. Vontobel identifies four key areas in particular where such progress is taking place: core technologies, automation, healthcare technology and consumer technology. A further advantage of the Vontobel Rising Economies Disruptors Index is the index sponsor’s comparatively high level of discretionary power. The sponsor is flexible when it comes to deciding on the respective index components and their weightings. As a result, the index is always optimally tailored to the strategy.

UBS China Tech ETF

Another interesting option is the UBS Solactive China Technology UCITS ETF (CQQQ). The benchmark index tracks the performance of the 100 largest technology-focused Chinese companies, which generate the majority of their revenue in various innovative business sectors such as cloud computing, medical technology, future mobility and digital entertainment. The index is weighted by free float market capitalisation, with a cap of 10% per share. As this is a total return index, dividends are reinvested. The index’s current heavyweights include consumer electronics giant Xiaomi and internet giants Tencent and Alibaba. Adjustments and rebalancing take place quarterly.

At ZKB, passive meets active

With a Tracker Certificate linked to the China Digital Economy Basket (JPCCDZ), Zürcher Kantonalbank is taking a somewhat unusual approach. The reason for this is that the basket is dynamically managed by the investment manager JP Cortesi Investments. Up to 50 adjustments may be made annually, with the manager able to hold up to 50% of the basket’s weighting in cash according to his assessment. The product is therefore an active structure disguised as a passive vehicle. It should be noted that, in addition to an annual fee of 0.35%, the investment manager retains 20% of the positive performance of the underlying asset as a performance fee. Furthermore, a fee of 0.10% of the transaction value is charged per rebalancing. Therefore, the investment is not exactly cheap.

Chinese Dragons for your portfolio

Leonteq’s Tracker Certificate on Swissquote China Dragons Index (CHINTQ) is designed to capitalise on China’s structural transformation. The index focuses, amongst other things, on future-oriented markets such as robotics, renewable energy and electric mobility, but also includes numerous companies from traditional sectors such as banking, aviation, industry and consumer goods. This broader exposure beyond the technology sector can be advantageous for diversification purposes, but it may also prove to be a a negative influence on returns. Particularly with regard to the heavily weighted banking stocks in the index, such as those of the Bank of China or China Construction Bank, the risks should not be underestimated.

Optimising returns with the internet trio

Finally, another product designed to optimise returns: the Multi Barrier Reverse Convertible (DDIBKB) by Basler Kantonalbank, based on the three Chinese internet stocks Baidu, Alibaba and JD.com, carries a coupon of 15.00% p.a. Redemption takes place at the nominal value of USD 1,000, provided that none of the three underlying assets touches or falls below its initially set barrier during the term until January 2027. Currently, Alibaba is 27.1% above the barrier, JD.com 34.7% and Baidu 37.5%. The main risk lies in a barrier event: if a share touches or falls below the barrier, this can lead to significant losses. The extent of the loss depends on the performance of the weakest underlying asset until maturity.