Opinion Leaders

Opinion Leaders

Geopolitics not igniting oil flare-ups

-

The Globe

Eurizon

Geopolitical tensions show no sign of easing, but the markets seem unfazed. How come? The answer to this recurring question lies in the low macro impact of current events, in turn explained by the low level (and low volatility) of energy commodities, with oil at the fore.

Unlike the outbreak of war in Ukraine, that had resulted in a reduction of gas and oil supplies, at the present stage there is a wealth of supply.

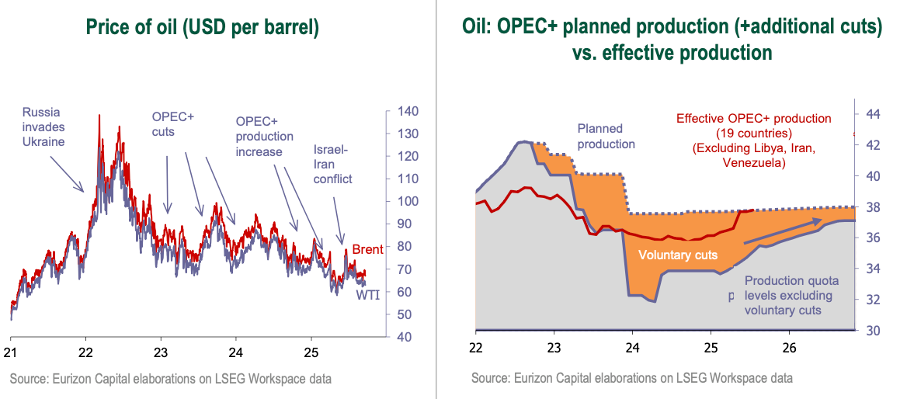

In truth, in 2025 oil prices incurred two tense phases, at the beginning of the year due to the sanctions imposed on Russia and the cold weather spat in the US, and in June, in correspondence with the Israel-Iran war, that soon came to an end. In these phases as well, however, the price of oil never exceeded 80 dollars per barrel.

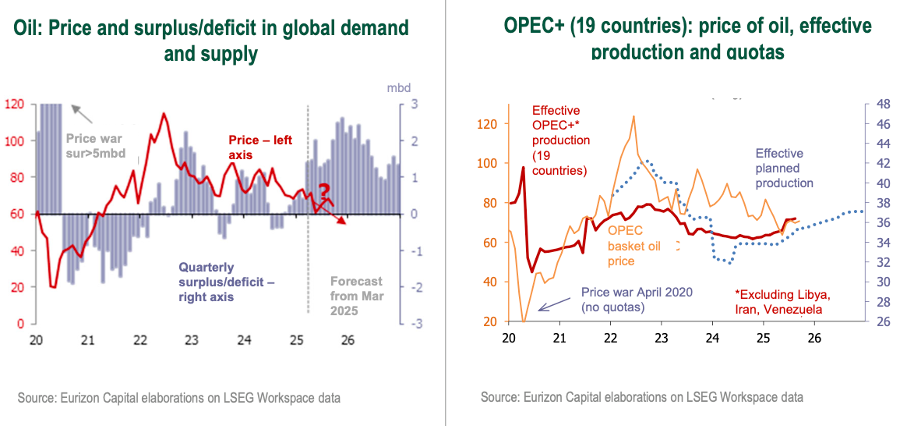

Since April, OPEC+ has changed its strategy, raising monthly planned production quotas. The initial intention was to step up production by 0.8 million barrels per day in the May-October period, whereas already in August the effective increase amounted to 1.3 million barrels. In doing this, OPEC+ absorbed half of the production cuts that had been decided in 2023.

With this production increase, OPEC+ has kept prices inside the USD 55-75 per barrel, managing to win back market shares without impacting the ideal balance for US profitability (below the 55 dollar mark, negative pressures emerge on US investments).

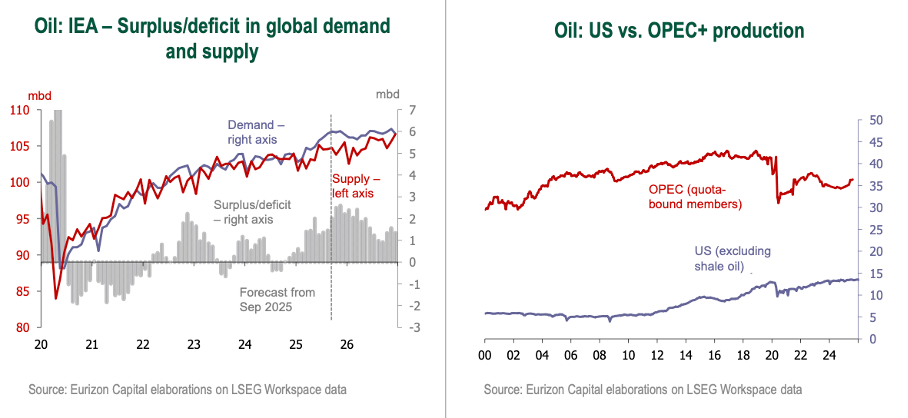

Going forward, according to the International Energy Agency (IEA), global demand will increase by 740k barrels per day as 2025 progresses, as opposed to higher supply by 2.7 million barrels per day (mbd), resulting in a surplus of in excess of 2 mbd.

OPEC’s estimates remain more optimistic, pointing to higher demand by 1.3 mbd driven by the Asian emerging markets. Actual consumption in China and India seems weaker than indicated by official forecasts, and several commentators believe OPEC are overestimating demand.

Albeit by different degrees, in the course of 2025 estimates of demand have been revised down, while OPEC production has increased, as also output in the US. Overall, prices seem to be heading for lower levels, rather than for a rise.

Therefore, the picture suggests that the balance between demand and supply is veering more significantly towards a structural supply surplus, compared to the opening months of 2025.

In the near term, prices will continue to be supported by purchases by China (that is stepping up its strategic oil stocks) and by the risks weighing on Russian production its strategic stocks. Analyst consensus, however, assumes that excess supply would result in prices falling towards the 50-60 dollar per barrel area at the beginning of 2026.

It should be stressed that this level still suit the Trump administration fine, as it aims to further push down inflation, but would be intended as a floor to not break through, or the profitability of US producers would suffer.

A delicate balancing act in containing inflation, safeguarding producer profitability, and neutralising the effects of geopolitical tensions.