Opinion Leaders

Opinion Leaders

Global profit growth for 2026 is expected to be 28%

-

Eurizon

Markets guided by three main themes: strength of the US economy, US-IRAN deal, and tech investment and earnings super-cycle.

US labour market data beat expectations for three consecutive months, after proving close to stagnant over the six previous months, thus proving the US economy’s extraordinary resilience to mounting energy prices, more than offset by the technology investment cycle. The US-Iran peace deal, which also provides for the reopening of the Hormuz strait, has pushed oil prices back down into the USD 75 per-barrel area. Given these circumstances, it is legitimate to believe that inflation may now have peaked. Money market futures are still pricing in the possibility of the Fed hiking rates slightly at the end of 2026, factoring in the strength of the economy. Also considered likely is a second ECB policy rate hike in the autumn, to fight inflation. The upward revision of corporate earnings growth estimates continued. At the global level, 2026 earnings are forecast at 28%, explaining the MSCI AC World index’s 12% or so appreciation in the first six months of the year. China is on the backburner: the impact of the Iranian crisis in the country was limited, both in fuelling inflation and in holding back economic activity

To date, 2026 has been a bumpy year, mostly for obvious geopolitical reasons. But what has been the impact on the markets’ macroeconomic outlook? We will try here to analyse the picture from the standpoint of the consensus estimates drawn up by economists, financial analysts, and the expectations implied by market prices.

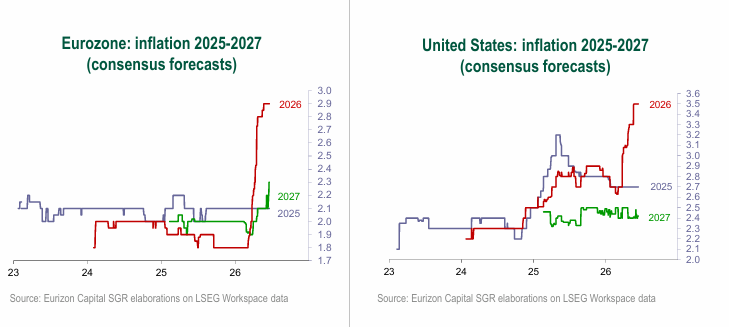

The defining factor in the first half of the year has been the impact of the war in Iran on oil prices stemming from the closing of the Hormuz strait, that significantly boosted inflation expectations.

In the Eurozone, at the beginning of the year 2026 inflation was expected stable at just under 2%, but was then revised up significantly, to around 3%. The revision of 2027 forecasts, on the other hand, was smaller, outlining the perceived temporary nature of the inflation shock.

Similar considerations apply to the United States, where inflation is now expected to average 3.5% in 2026, up from 2025, but forecast to return to levels not far off the 2% mark in 2027, again revealing expectations for a temporary inflation shock.

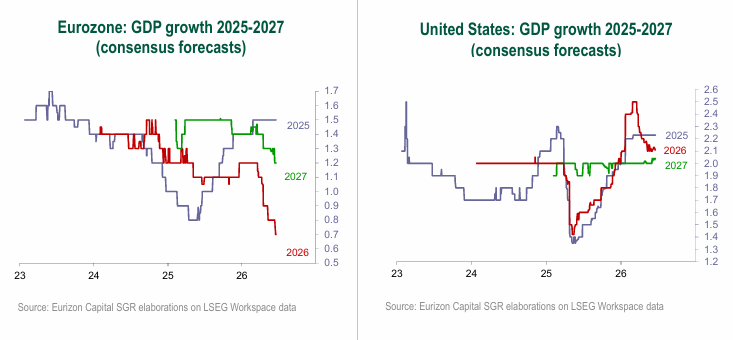

For what concerns growth, while still within the context of an ongoing global economic cycle, forecasts have been lowered due to the oil shock resulting from the geopolitical tensions.

In the Eurozone, growth estimates were revised rather sharply due to the stronger impact of the effects of the crisis on economic activity than in the US, given Europe’s greater dependency on commodity imports.

Average growth in the Eurozone is forecast at less than 1% in 2026, roughly half the 2025 reading, with a moderate downward revision of expectations for 2027.

In the United States, the picture seems more resilient, as the impact of geopolitical tensions is outbalanced by the structural technology investment cycle and by a revived labour market.

Therefore, the downward revision of growth expectations for the U.S. economy in 2026 has proven more limited than for the European economy, and growth is in any case expected to stay at around 2%, in line with both 2025 and with forecast for 2027.

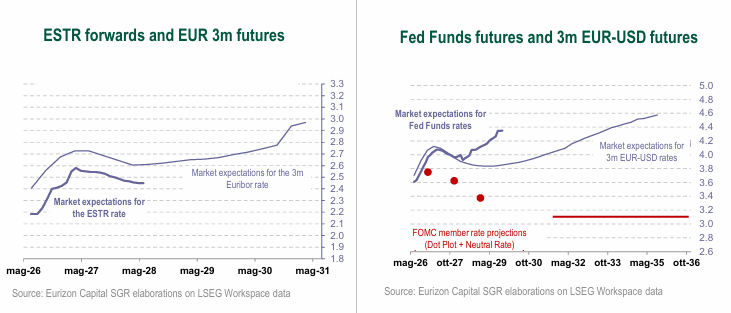

The increase in oil prices and the resulting growth of inflationary pressures have also had an impact on the monetary policy decisions of the major Central Banks.

In Europe, despite contained economic growth with the added negative impact of the energy shock, the ECB has focused on inflation risks and on its second-round effects, hiking rates in June from 2% to 2.25% (deposit rate).

The market is ready to price in a further rate increase in the course of this year, although much will depend on the trend of oil prices following the agreement reached by the US and Iran to reopen the Hormuz strait.

For what concerns the Fed, the expectations for a rate cut that were in place at the beginning of the year, before the US-Iran war, have been put on hold for 2026. In the present phase, a solid macroeconomic picture, the recovery of the labour market, and accelerating inflation due to the energy shock have advised the Fed to revise slightly upwards its policy rate projections.

Money market futures are more focused on the strength of the economy than on inflation fears and outline a potential need for an upward adjustment of rates around the end of 2026 to prevent the economy from overheating.

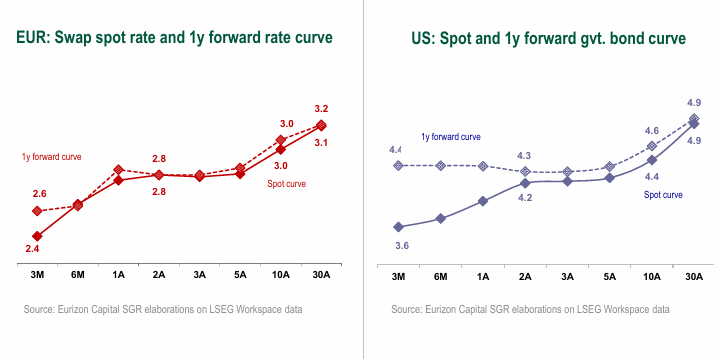

For what concerns the bond markets, forward rates allow us to look ahead to the future, as the shape of their curves imply expectations for the future course of interest rates.

The euro curve, with short-term rates close to 2.6%, long-term rates (10 years) at 3%, and a one-year forward curve positively sloped with rate levels essentially in line with the current, suggest that the markets have already priced in a potential new ECB hike, without expressing significant fears neither of a further deterioration in growth, nor of an additional acceleration of inflation.

The US curve, with short-term rates at 3.6% and the longer maturities (10 years) at 4.5%, and a slightly flattened one-year forward curve, with short-term rates higher than at present, is pricing in a policy rate increase by the Fed prompted by the strength of the US economy. The fact that longer maturities are seen to stay at levels close to their present ones reflects the effectiveness of the Fed’s move in curbing inflation.

These expectations would allow investors to cash in the coupon flows offered by the bond markets and to achieve capital gains in case of an unexpected slowdown of the macroeconomic cycle (anti-recession insurance policy).

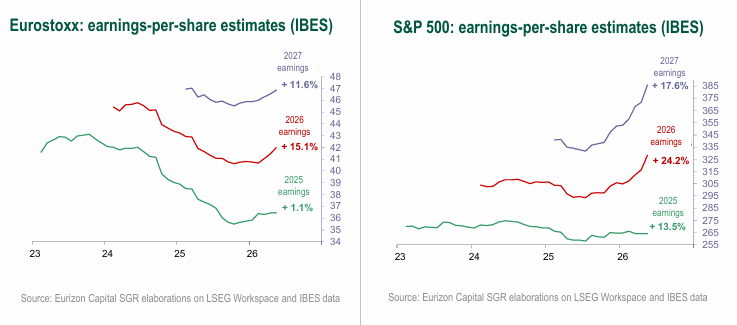

Despite to the geopolitical tensions and the deterioration of growth estimates, in the first half of 2026 corporate earnings estimates were revised up sharply.

In the Eurozone, Eurostoxx index earnings are forecast higher by 15% in 2026, after stagnating in 2025 due to tariffs, and are also expected to grow in 2027, albeit at a slower pace than in the US and in the other regions in which the technology sector weighs more.

In the US, S&P 500 index earnings are estimated to grow by 24% in 2026 compared to 2025, and to subsequently rise by 18% in 2027, supported by the structural technology sector investment cycle.

At the global level, 2026 earnings growth is forecast at 28%, which explains the increase of around 12% achieved by the MSCI AC World index in the first six months of the year.

This is a solid earnings growth cycle, supported by investment in technology and artificial intelligence, which has allowed the economy and the stock market to offset geopolitical tensions and rising energy prices.