Trading Desk

Trading Desk

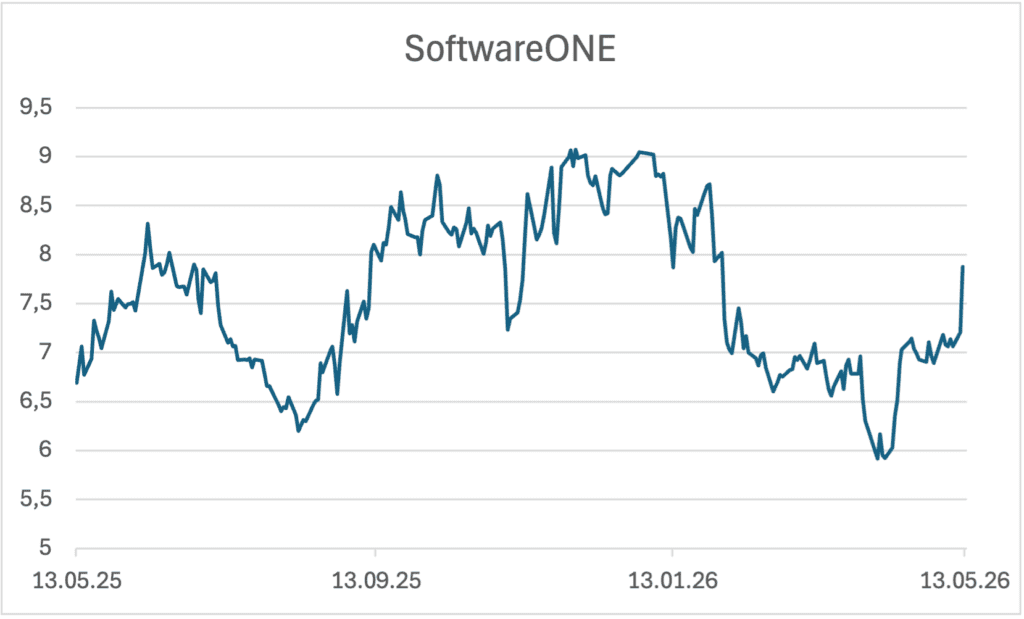

SoftwareONE: Restart picks up speed

-

Christian Ingerl

Redaktor

Strong sales growth, rising margins and progress with the Crayon integration are giving the share a new boost. With tailwinds from the cloud, AI and cost synergies, the turnaround could now gain substance.

After the transition year 2025 SoftwareONE started the new financial year with astonishing momentum. What still looked like integration work, strategic reorganization and a test of patience in the previous year increasingly looks like the start of an operational turnaround after the figures for the first quarter of 2026. The share, which came under further pressure at the start of the year, has already fallen by more than a third from its low. Following the jump in the share price after the presentation of the figures, the high for the year is now back in sight. The technical chart picture has thus brightened noticeably. Fundamentally, the Stans-based company is now providing the arguments for this.

Positive synergy effects

Although the provider of software and cloud solutions made significant progress last year, the year was clearly characterized by restructuring. The acquisition of Crayon, the integration of the new structures and adjustments to supplier incentives had a negative impact on perception on the capital market. At the same time, the company managed to achieve sales growth of 1.4% on a combined comparable basis, exceeding its own expectations of a rather flat year. The adjusted EBITDA margin was 20.9% in 2025. More importantly, the company showed that the synergy targets from the Crayon integration are not just theoretically achievable. Cost synergies of CHF 43 million had already been realized by the end of 2025 and CHF 64 million by mid-March 2026.

The momentum has now accelerated significantly at the start of the year. On a comparable combined basis, currency-adjusted sales rose by 12.9%. This means that SoftwareONE not only clearly exceeded its own annual target, but also exceeded market expectations. Particularly positive: growth was broad-based. All business areas and regions contributed to the improvement. Even the NORAM region, which was considered a problem child in previous quarters, got back on track with currency-adjusted growth of 10%. This is more than just a side note. After all, SoftwareONE had previously been struggling with internal sales problems in North America in particular. The fact that this region is now turning around increases the credibility of the management.

Margin improvement

The direction is also right on the earnings side. Reported EBITDA increased by CHF 44.3 million to CHF 71.0 million in the quarter and the EBITDA margin improved by 3.4 percentage points to 20.5%. The synergies from the Crayon integration are therefore beginning to have a visible impact. At the beginning of May, the annual cost synergies already amounted to more than CHF 80 million. SoftwareONE is therefore on track to reach the target of CHF 100 million by the end of 2026. It is precisely this operating leverage that is crucial for the share: if sales growth and margin expansion come together, the earnings profile can improve rapidly.

Accordingly, SoftwareONE has raised its outlook for 2026. Instead of mid single-digit revenue growth, the company now expects mid to high single-digit growth at constant exchange rates on a comparable combined basis. The forecast for the adjusted EBITDA margin of more than 23% has been confirmed. The dividend policy also remains attractive: a dividend ratio of 30% to 50% of adjusted annual profit is still planned.

Opportunities and risks

The growth opportunities extend beyond pure cost synergies. SoftwareONE is benefiting from several structural trends. The most important is the ongoing shift from traditional license models to cloud subscriptions and usage-based solutions. Added to this is the AI boom. Artificial intelligence is not just a short-term buzzword for the company, but a concrete demand factor. Services relating to cloud migration, cybersecurity, data management, FinOps and managed services appear particularly promising.

This paints a very positive picture for the share. Operational growth is picking up, margins are rising, integration is delivering and the medium-term drivers of cloud, AI and services point to a sustained improvement. Risks remain: Competition is intense, the business is heavily dependent on partners, particularly Microsoft, and weaker IT demand could slow down the upturn. At the same time, SoftwareONE must continue to build up its credibility after the disappointments of the past. The first quarter was an important step in this direction.

Investment solutions

If the momentum from the first quarter can be maintained, the share should also have further upside potential. For risk-conscious investors, SoftwareONE therefore remains an exciting turnaround stock with growing operational substance. For a short to medium-term upward speculation, the Mini Future ISWJSZ of the ZKB. The leverage is 3.4, the knock-out is 27.2% away from the current level. The Mini Future long has even more “tinder” MSWA6T from Leonteq. This endless product multiplies the price performance by a factor of 5.8, the knock-out is 15% away from the current underlying price.

However, attractive returns are also possible with a sideways product. The Barrier Reverse Convertible SBUGJB from Julius Baer offers the prospect of a return of 16.2% until the beginning of 2027. This high return is hedged with a risk buffer of more than one third. The barrier is set at CHF 5.30.