Opinion Leaders

Opinion Leaders

The Globe – Global Outlook 2026

-

Maria Luisa Gota

Chief Executive Officer and General Manager

Eurizon

A Prolonged Global Economic Cycle underpins a Constructive Market Scenario

“2026 opens under the banner of continuity for the global economy: growth, fiscal and monetary policies oriented toward stabilization define Eurizon’s central scenario, against a backdrop of geopolitical uncertainty,” said Maria Luisa Gota, Chief Executive Officer and General Manager of Eurizon. “In this context, quality, diversification and professional management remain the key pillars for navigating a cycle that, while mature, still delivers value.”

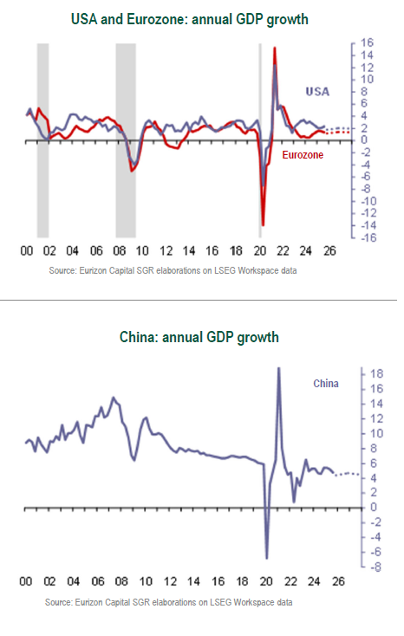

2026 is perspective to be a year of ongoing global economic growth, the seventh in the post-Covid cycle. There are at least three reasons to take this as the baseline scenario.

Fiscal policy is moderately expensive in the US and will support economic activity in the Eurozone, thanks to the defence and infrastructure spending plans.

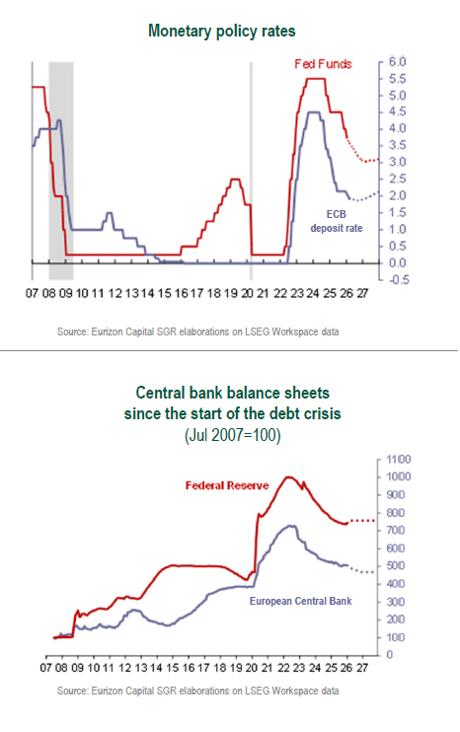

Monetary policy is expected to be kept neutral in the Eurozone, where rates are already in line with inflation, and will turn neutral in the US as the Fed’s rate-cut cycle continues.

2026 will be an election year in the United States, as the Midterm elections will be held in November. The Trump administration will therefore aim to prevent economic turbulences in the year.

For what concerns China, the economic authorities are dosing stimulus calibrated fashion to keep growth in line with the 5% y/y target. In this sense, China represents an element of stabilisation for global growth.

Risk scenarios, unlikely to materialise, include a potential “macro disappointment” in the United States tied to persistent labour market weakness, or to the slowdown of investment in artificial intelligence (AI). In the Eurozone, risks could include delays in the implementation of the defence and infrastructure spending plans. A weak macro picture would be balanced by both the Fed and the ECB taking more markedly accommodative monetary policy stances.

On the other hand, an alternative scenario of stronger economic growth than expected by the markets would imply less accommodative central banks, while corporate earnings would undoubtably benefit.

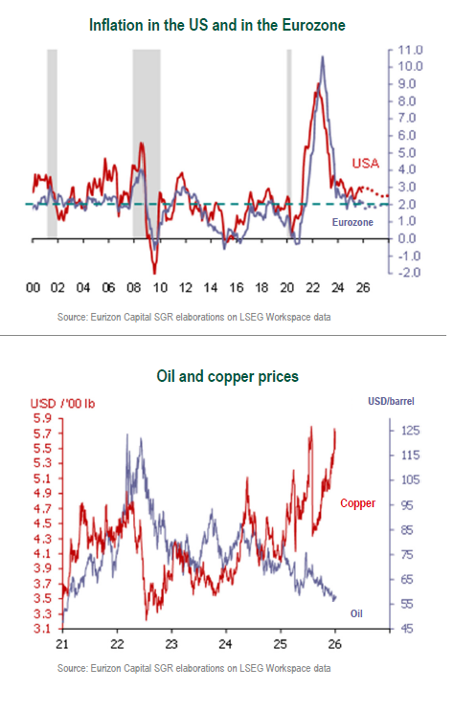

One positive factor to consider is the stability of inflation. In the Eurozone, its return to 2% is now consolidated. For what concerns the US, the introduction of trade tariffs on imports has failed to reignite inflation as the tariffs were largely taken on by businesses, with a modest fallout on consumer prices. US inflation has stabilised at just under 3%, slightly higher than in the pre-Covid period.

In 2026 the central banks may largely stay on hold

While it is true that the Fed is still in the process of bringing monetary policy back to neutral, an inflation rate stably back at just under 3% means that only two further cuts are needed to reach the target rate. According to the baseline scenario, the Fed will make these cuts in the central months of the year and subsequently stay on hold in a neutral position.In this sense, the main focus theme on the Federal Reserve front will be the change at the helm, as Powell’s mandate will end in May. The name of his successor well in all likeliness be announced well in advance.The ECB has already brought rates to neutral, with the eight cuts made between June 2024 and June 2025. According to the baseline scenario, it should keep monetary policy unchanged throughout the year.The ECB is still in the process of shrinking its balance sheet (Quantitative Tightening), balancing the Quantitative Easing measures introduced starting in 2008 and then after Covid. The Fed has already put Quantitative Tightening on hold, while the ECB seems set on pressing on this year, possibly completing the process in 2027.