Opinion Leaders

Opinion Leaders

Redefining a Value Strategy for Global and Japanese Portfolios

-

Shirley Low-Storchenegger, Head of Asia/Pacific

MUTB’s Satoshi Sakamaki discusses a new family of indices that seek quality value companies for higher and stable returns.

STOXX continues to expand the iSTOXX MUTB smart-beta index family with Mitsubishi UFJ Trust and Banking Corporation (MUTB) of Japan, following the successful roll-out of the iSTOXX MUTB Quality indices. This time we have jointly developed an innovative approach to value investing.

The iSTOXX MUTB Value indices select companies from the STOXX® Global 1800 and the STOXX® Japan 600 indices based on a normalized value factor captured by three ratios: book to price, earnings to price and cash-flow from operations to price. A previous step screens out companies with high price and earnings volatility from the benchmark universe, to avoid so-called ‘value traps.’

The new indices are the iSTOXX® MUTB Japan Value 300, iSTOXX® MUTB Global Value 600 and iSTOXX® MUTB Global ex Japan Value 600. They are designed to underlie different types of financial products, including exchange-traded funds.

Extracting quality value premium

Value risk as a return driver is one of the most widely studied factor premia. Besides the distinctive use of more than one valuation ratio to come up with a higher-quality portfolio of value stocks, companies with high price volatility, and high accruals (or low-quality earnings), are filtered out, improving the stability of the portfolio’s asset value and securing the accuracy of valuations.

A multi-factor definition of value may lower portfolios’ volatility and expose them to a more diversified source of returns than would a single-factor approach. Additionally, research shows that a composition of more than one value factor outperforms any single value factor in the long term, likely due to the diversification and low volatility characteristics.1

Stocks in the iSTOXX MUTB Value indices are ranked and weighted by their normalized value score. The factor is adjusted to account for regional and industry specific biases. For more on the index methodology, please click here

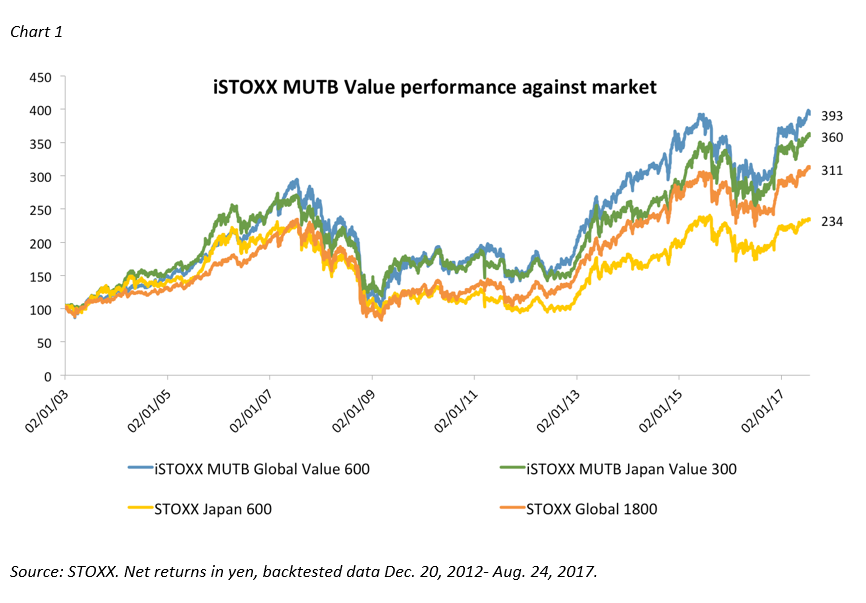

Chart 1 shows the backtested performance of two iSTOXX MUTB Value indices – Global Value 600 and Japan Value 300 – against their respective market-weighted benchmarks.

We talked to Satoshi Sakamaki, senior deputy general manager at MUTB’s asset-management division, to learn more about the rationale and objective of the new indices.

What makes the iSTOXX MUTB Value indices an interesting proposition for global- and Japan-focused investors at this time?

Value is an effective factor recognized all over the world that has also been confirmed by many academic papers. In Japan, especially, the value effect has had high performance over a long period of time. We believe the iSTOXX MUTB Value indices meet the demand of investors who would like to achieve the risk-reward of the value factor over the long term. Here, we consider that the investment efficiency in the practical application of a factor strategy is important and determinant for results.

That leads me to the next question. The iSTOXX MUTB Value indices have a distinctive approach to selecting stocks. They employ a normalized value factor that collects from not one, but three ratios. Can you explain the rationale behind this strategy and what sort of long-term performance can be expected from it?

The relationship between share price and the shareholders’ value of a corporation is a key factor. The iSTOXX MUTB Value indices select companies based on a normalized value factor that is captured by the ratios of book to price, earnings to price and cash-flow from operations to price. Our studies show that these three fundamental indicators have proved to be effective in capturing a company’s real value. That said, the timing when each indicator is rewarded or gains preference in the market, differs. And therefore the returns effect coming from each indicator depends on the point in the business cycle. For example, if expectations are for the market or the economy to rise, then a potential increase in the profits earned by a company is likely to be reflected in the share price. On the other hand, if investors are discounting the possibility of an economic recession, a decrease in profits and even losses will be expected. In that case, companies with stable net assets will be rewarded foremost.

As another example, having adequate cash flow, which represents the flexibility of corporate structure, is something that is highly rewarded in times of crisis for a given business model.

A screening that combines these three indicators results in the selection of stocks that are expected to maintain a reasonable and relatively stable profit stream throughout the whole business cycle. I’ll add here that the index components are weighted according to the calculated value factor score that combines all three indicators.

There is also consideration on volatility and a preference for companies with low levels of accruals. Why is that?

Indeed, the screening method allows us to increase the efficiency of the value strategy. The two additional screening factors of accrual and stock-price volatility are likely to enhance the accuracy of evaluating a stock’s fundamental value. Therefore they help achieve a better value approach.

Accruals, in particular, can act as window-dressing for a company. They undermine a reliable analysis of the fundamental value of a company and can hence push investors to allocate resources to ‘value traps.’ If the accrual is low, then we can consider that the company produces high-quality cash profits. On the contrary, if the accrual is high, then its profit is low quality, and the reliability of the estimated fundamental value is low.

Are the iSTOXX MUTB Value indices geared towards any particular segment of the investor base?

The iSTOXX MUTB Value indices take into account the liquidity needed by institutional investors. We believe then that all kind of investors will find them suitable and appropriate as investment vehicles.

1 ‘An Overview of Factor Investing,’ Fidelity Investments, September 2016.

Featured indices

iSTOXX MUTB Japan Value 300

iSTOXX MUTB Global Value 600

iSTOXX MUTB Global ex Japan Value 600