Trading Desk

Trading Desk

Givaudan: Share with new fragrance

-

Christian Ingerl

Redaktor

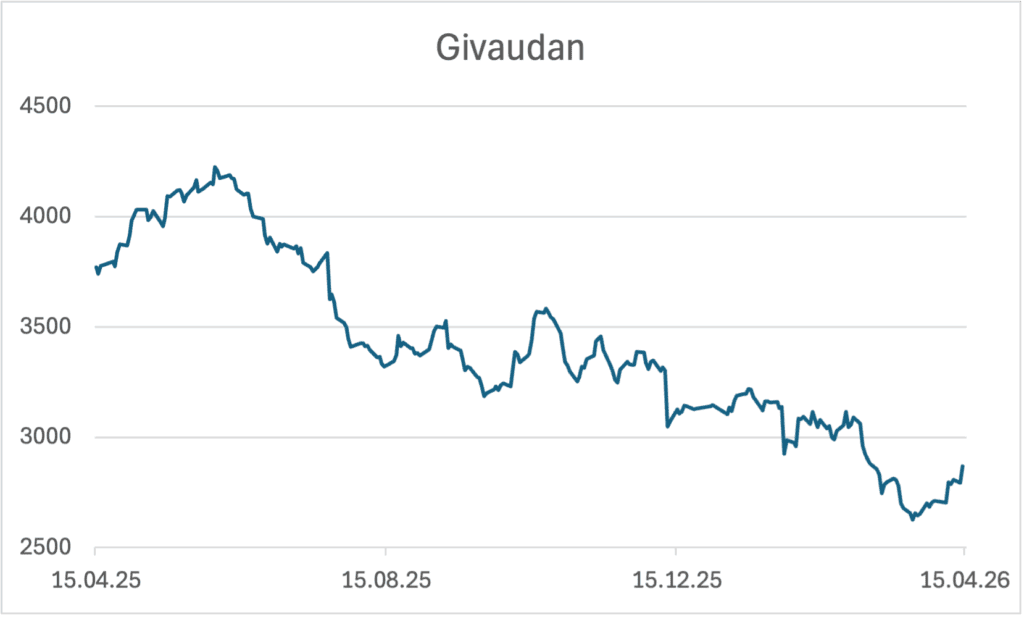

Givaudan has recently shown signs of life again on the stock market. A surprisingly solid set of figures is fueling hopes of a turnaround. This could open a window for investors in which operational stability meets a comparatively favorable valuation.

The Givaudan share has had a difficult time in recent months. After peaking at over CHF 4,200 in June 2025, the stock came under increasing pressure, weighed down by weaker expectations, currency headwinds and a general cooling of valuations in the sector. Now, however, there are increasing signs of a cautious comeback attempt, with the share trading around 12% lower just a few weeks ago.

Better than expected

A new impetus came with the figures for the first quarter of 2026, which were well received by the market: On the day of publication, the shares rose by more than 5% at their peak, significantly outperforming the market as a whole. The reaction is an expression of a certain relief – and perhaps also of renewed confidence in the operational strength of the flavor and fragrance manufacturer. Operationally, the picture is varied: sales in growth markets rose by 4.0%, in established markets by 1.7%. Overall, Givaudan achieved organic growth of 2.8% in the first quarter, which was below the long-term target range of 4% to 6% and marked a further slowdown compared to the previous quarter. However, the decisive factor is that expectations were exceeded. On average, analysts only had 1.7% on the cards. In an environment of subdued forecasts, a “beat” like this is enough to turn perceptions around.

A look at the details underlines this assessment. The fragrance business in particular – traditionally a high-margin area – performed better than expected. Growth was driven primarily by consumer goods applications and the luxury fragrances business. Demand here appears to have remained robust despite a high basis for comparison. In contrast, the Taste & Wellbeing segment was less dynamic, declining slightly. Overall, the picture is one of stability rather than weakness.

Thumbs up

Analysts have a correspondingly constructive view of the figures. Vontobel emphasizes that the industry has recently suffered from a significant cooling of valuations. Against this background, the current results are an indication that Givaudan’s business model continues to work. According to the analysts, the current valuation therefore appears too pessimistic. UBS also views the figures positively. In particular, the big bank emphasizes the strength in the fragrance business. The experts see this as a signal that Givaudan continues to have pricing power and innovative strength in its core segments. Kepler, in turn, sees more positive sales growth in the second half of the year. As usual, the company itself does not provide an outlook for the current year, but confirms its targets for the strategic period 2030, where average sales growth of 4% to 6% is expected.

In terms of valuation, the Givaudan share is at a historically low level, which could open up room for upside potential. This is also the core of the current investment story. The Group is not growing spectacularly, but solidly – and better than feared. At the same time, most of the risks are probably already priced into the share price. If the company succeeds in stabilizing growth over the course of the year and defending its margins, the discrepancy between operating reality and valuation could close further.

Investment solutions

After a long period of weakness, there are signs of a turnaround both operationally and on the capital market. It is still too early to speak of a sustained upward trend. However, the latest figures provide arguments that the comeback attempt of the Givaudan share could be more than just a short-term recovery. Anyone wishing to bet on an upward trend in the share price can do so with the Long Mini Future PGIVFU from UBS. The product has a leverage of 4.7, the knock-out is at CHF 2,329.4060 and thus a reassuring 19.2% away from the current price. Leonteq’s MGID0T product offers even greater opportunities, but is also riskier. The higher leverage of 7.3 comes at the expense of the buffer. The barrier at CHF 2,549.7350 only allows a setback of 11.5% before the product expires worthless.

The Barrier Reverse Convertible RGIADV from Bank Vontobel is ideal for conservative investors. The product currently offers the prospect of a return of 13.7% p.a., with a solid risk buffer of 16.6%. The term ends on 22.01.2027.