Trading Desk

Trading Desk

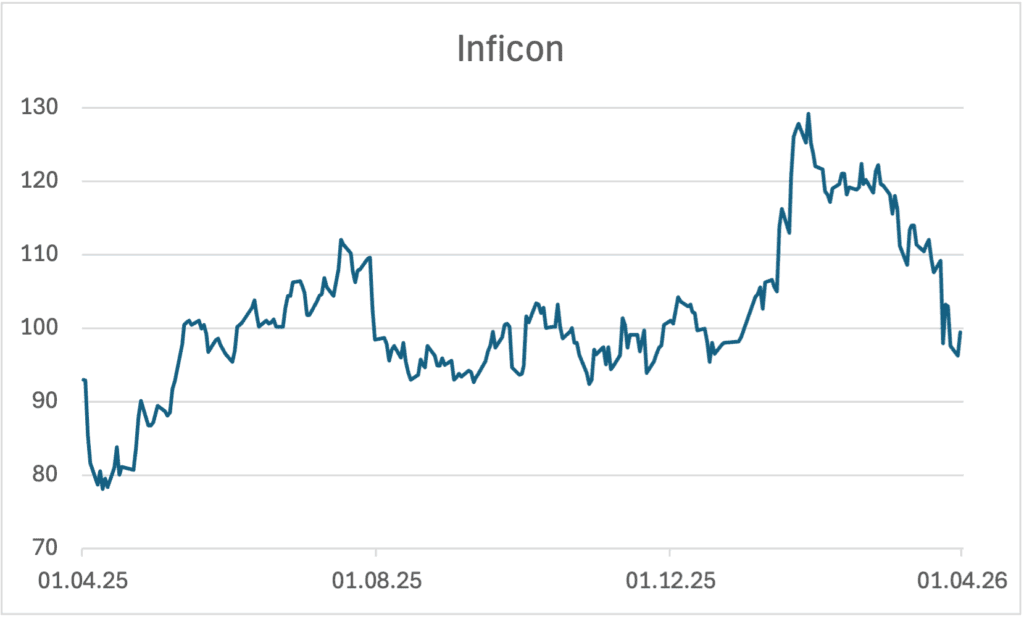

Inficon: Chip profiteer struggles to reach the 100 mark

-

Christian Ingerl

Redaktor

The measurement technology specialist is well positioned in structurally growing markets. The current consolidation of the domestic small cap could prove to be a favorable entry opportunity in retrospect – both in the short and medium term.

The euphoria has faded – at least for the time being. After the share of Inficon shares had been on a solid upward trend for months, disillusionment followed recently: a significant setback pushed the price back towards the psychologically important CHF 100 mark. Investors are now wondering whether this is the end of the rally – or rather the beginning of a new entry opportunity.

Mixed number ring

The correction was triggered by the recently published figures for the 2025 financial year and a cautious outlook. In operational terms, the picture was mixed: sales largely stagnated at around USD 674 million, while profit fell significantly after a strong previous year. Adjusted net income fell to USD 85.8, which corresponds to a decline of almost a quarter. This was due in particular to exchange rate effects, higher costs as part of the realignment of the production structure and tariff-related effects, which reduced the operating margin by more than 300 basis points.

However, looking ahead puts the short-term weakness into perspective. Inficon is forecasting sales growth of 1% to 7% for 2026 – a range that was initially received as disappointing by the market. However, the focus is less on the dynamics and more on the quality of growth. While traditional areas such as automotive or parts of the general vacuum business are currently weakening, the core business relating to semiconductors and vacuum coating is in remarkable shape.

Growth strategy

This is precisely where the structural drivers lie: demand from the semiconductor industry is picking up again, supported by increasing investment in new production capacities. Inficon is benefiting from the increasing “vacuum intensity” of modern chip production – a trend that should ensure rising margins and sales in the long term. Accordingly, analysts expect incoming orders to accelerate as early as 2026. There are also many signs of a turnaround on the earnings side. A significant increase in profits is forecast for this year, with earnings before interest and taxes (EBIT) expected to grow by almost a fifth. The operating margin should gradually move back towards the targeted level of over 20% as soon as the temporary burdens come to an end.

Strategically, Inficon remains well positioned: The company has strong market shares in several niches, a broad customer base and solid innovation capabilities. In addition, the robust balance sheet allows for largely self-financed expansion. At the same time, the diversification across various industries ensures a certain resilience to cyclical fluctuations.

Investment solutions

Against this backdrop, the recent share price weakness appears to be less a structural problem than a classic overreaction to the more cautious tones coming from Group headquarters. ZKB analyst Michael Inauen brings another reason for the management’s caution into play: the upcoming change of CFO in June. The guidance may therefore have been deliberately cautious. In fact, analysts continue to see considerable potential: the average 12-month price target is CHF 118.50, which implies an attractive premium of more than a fifth from the current level. From a technical chart perspective, it is now important for the small cap to defend the CHF 100 mark. For this endeavor, the Inficon share has an important support zone in the CHF 90/100 range at its disposal, which proved its validity for months last year.

Investors who would like to bet on a turnaround above the psychologically important level after the consolidation can invest in the Long Mini Future MIFAMT from Leonteq. The leverage product offers a multiplier of 5.7 and thus benefits disproportionately from rising prices of the underlying. The knock-out is located at CHF 87.7018. However, if the outlined support does not hold, a short speculation comes into play. The mini future IIFFBZ from the ZKB. The stop-loss level is at CHF 110.4345, which conversely means a gap of a good tenth.

In the event of a sustained consolidation at the current level, the Barrier Reverse Convertible SCEBJB from Julius Baer with a remaining term of just under one year can be considered. The product offers the prospect of a double-digit percentage return of 13.8% p.a., with a barrier at CHF 62.75 – a buffer of just under 37%.