Trading Desk

Trading Desk

Roche: New fantasy in the pipeline

-

Christian Ingerl

Redaktor

The world’s largest cancer drug manufacturer is back with new impetus: data from the obesity portfolio, a billion-euro deal in cancer research and progress at Tecentriq. This presents opportunities for both traders and conservative investors.

Earlier this week Roche invited its investors to a virtual update on the American Diabetes Association. At “Roche’s Virtual ADA Investor Event”, the focus was on a topic that has long been one of the great hopes of the pharmaceutical industry on the capital markets: Obesity. New data was presented on two drug candidates with which the Group intends to attack the multi-billion dollar market for weight loss therapies. The focus was on enicepatide, formerly known as CT-388, and petrelintide, an amylin active ingredient from the partnership with Zealand Pharma. The event was a signal to the market that the long-criticized pipeline could regain clout.

Hopeful data…

Analysts believe that enicepatide in particular could prove to be a competitive GLP1 agent. Phase II data showed a weight loss of 22.7% at the highest dose after 48 weeks. Experts therefore expect that the substance could even achieve values of well over 25% in Phase III. If this is successful, Roche would be in the range of the efficacy profile of established blockbusters such as Eli Lilly’s Zepbound.

…and promising deals

At the same time, Roche is also working on strengthening its pipeline in oncology. The latest billion-euro deal with Nurix Therapeutics attracted a great deal of attention. Roche secured an exclusive license and collaboration agreement for the development of Bexobrutideg, an experimental drug against various blood cancers. The agreement could be worth up to USD 2.3 billion. Nurix will initially receive USD 700 million, while the remaining development costs will be borne 40% by Nurix and 60% by Roche. Phase III trials are scheduled to start in the summer. For Roche, the move is strategically logical: the Group wants not only to defend its strong position in cancer medicine, but also to expand it with new mechanisms of action.

The fact that Roche continues to have operational clout in this field was demonstrated just a few weeks earlier. The US Food and Drug Administration (FDA) granted further approval for the cancer immunotherapy Tecentriq, also known as atezolizumab. The drug can now be used in the USA as an adjunct in patients with muscle-invasive bladder cancer following removal of the bladder. This is already the eleventh indication for Tecentriq in the USA. This is not only a medical success, but also a commercial stabilizer: Tecentriq achieved sales of a whopping CHF 3.6 billion in 2025.

The Group has also recently made its mark outside of traditional drug research. With the planned acquisition of the US company PathAI for up to USD 1.05 billion, Roche is strengthening its diagnostics division. PathAI specializes in AI-supported tissue analyses. Roche wants to use it to make cancer diagnoses more precise and accelerate the development of new therapies.

Robust start to the year

Roche’s operating performance was robust at the start of the year: although sales in the first quarter were slightly below consensus expectations, this was mainly due to stronger negative currency effects. On a constant currency basis, Group sales grew by six percent and were thus even slightly above analysts’ expectations. The Pharmaceuticals Division grew by seven percent on a constant currency basis, while Diagnostics grew by three percent. Most importantly, Roche confirmed its outlook for 2026, with sales expected to grow by a mid-single-digit percentage at constant exchange rates and core earnings per share by a high-single-digit percentage.

Investment solutions

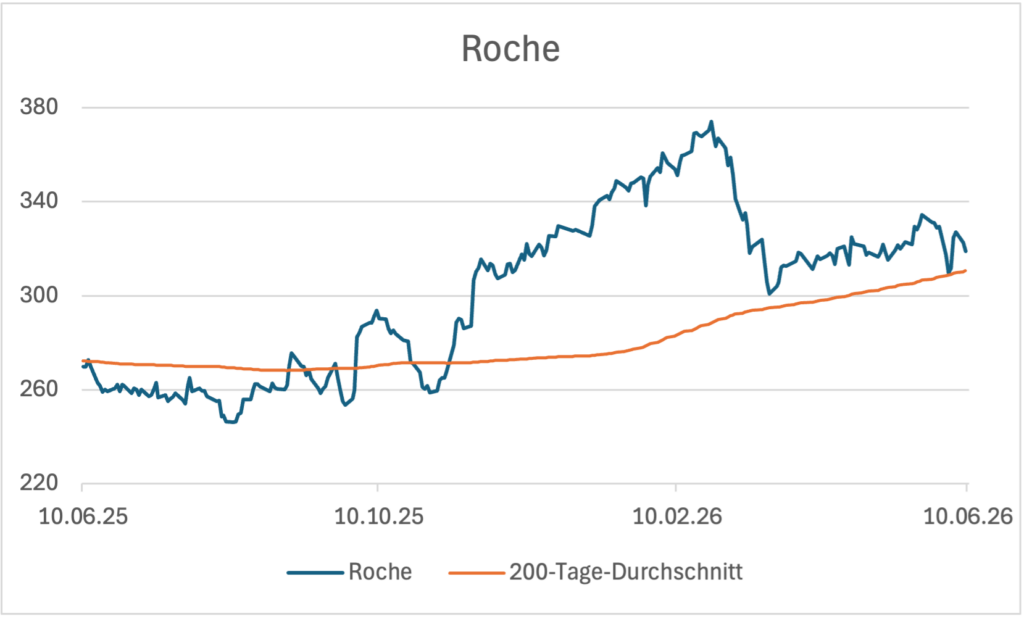

After a strong run until the end of February, Roche’s non-voting equity security entered a consolidation phase that brought the SMI share down to CHF 300. However, the latest news shows that the Group’s operational and strategic prospects are looking promising again. The share price has also recently headed north again. Risk-tolerant investors can leverage a possible comeback with long derivatives. The long mini future BFWSPU from UBS. The product has a leverage of 4.0 and the knock-out is at CHF 243.4606, which is 24% away from the current price. The Mini Future offers even more leeway on the downside MROAZT from Leonteq. The stop-loss level is at CHF 224.7958, which conversely means a distance of just under 30%. The leverage is 3.3.

However, conservative investors can also bet on Roche climbing with a bonus certificate. The product SAMXJB from Julius Baer offers the prospect of a return of 8.70% in the event of a sideways movement. If the underlying share price rises above the bonus level of CHF 350, the structured certificate participates 1:1 in any increase. The sideways return is in turn protected by a risk buffer of one tenth.