Trading Desk

Trading Desk

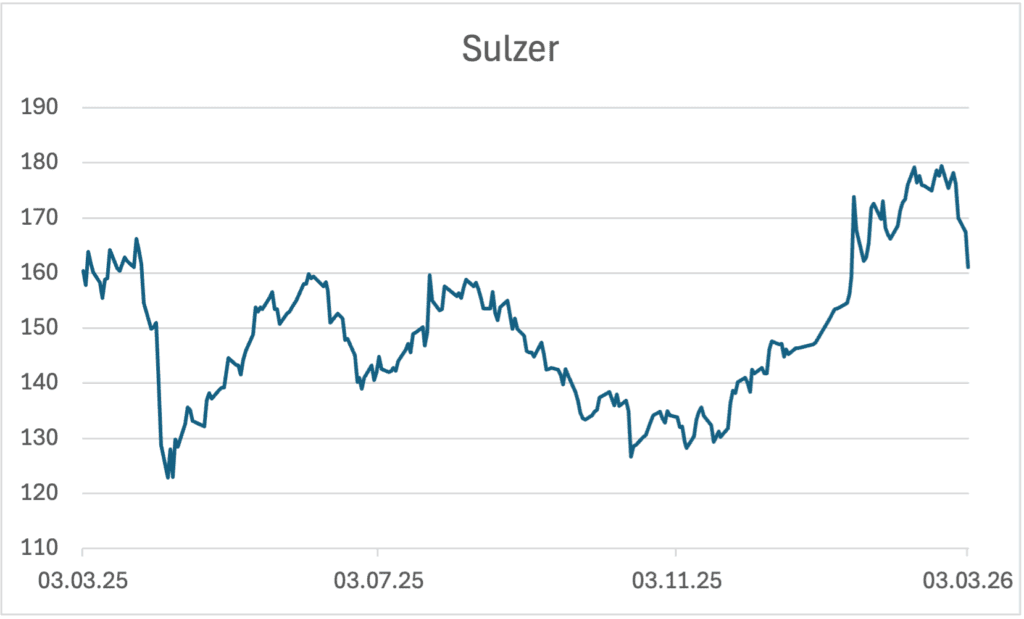

Sulzer: Record broken, breath taken

-

Christian Ingerl

Redaktor

Barely on record course, already under pressure: after strong figures for 2025, the share saw profit-taking. But operationally, things are going well: higher margins, robust order quality and a confident outlook for 2026 suggest an interim correction rather than a change in sentiment.

Just a few days ago, the Sulzer seemed to know only one direction: upwards. With the jump to a new record high, the industrial group crowned an impressive share price rally in recent months. This made the subsequent setback following the presentation of the business figures for 2025 all the more surprising. But a closer look quickly reveals that the correction was less an expression of operational weakness than the result of classic profit-taking after a strong share price performance.

Strong growth year 2025

In operational terms, Sulzer delivered a convincing set of figures: order intake increased organically by 2.1% in 2025, driven by a significant upturn in the final quarter. In the fourth quarter alone, orders amounted to CHF 974 million, an increase of 7% compared to the previous year. Sales grew organically by 5.6%, while profitability increased even more dynamically: EBITDA improved by 18% to CHF 556.2 million, increasing the margin by 140 basis points to 15.6%. The operating strength was also evident at the bottom line: earnings before interest and taxes rose by 22.1%, net profit climbed to CHF 294.7 million and the return on capital employed (ROCE) reached a solid 21.1%.

The qualitative change in the business is particularly striking. Sulzer is consistently focusing on price discipline instead of volume growth. The gross margin in order intake rose to 35.7% – a sign that management is increasingly avoiding lower-margin projects. The main drivers of this development were the Flow division and the robust service business. The latter once again shone with double-digit growth and an EBITDA margin of 18.3%. By contrast, the environment in the Chemtech business remained much more difficult, suffering from overcapacity in China and a weak chemicals economy.

Confident outlook

Looking ahead, the picture remains constructive. Despite geopolitical and macroeconomic risks, Sulzer is forecasting moderate growth for 2026: order intake is expected to increase by 1% to 5% and sales by 2% to 5% percent. More decisive, however, is the margin development. The company expects a further improvement in the margin to around 16.5%. Analysts see this as confirmation of the strategic transformation towards a margin-driven industrial company with a high aftermarket share and stable visibility.

In operational terms, the new year is likely to be divided into two halves. Due to high comparative figures from 2025, the first half of the year could be rather subdued, while a strong project pipeline suggests a much more dynamic second half. In the medium term, observers believe Sulzer is capable of even more: an EBITDA margin target of over 17% could be achieved as early as 2027, and in the long term even figures above the 20 mark appear conceivable.

Breathing space instead of trend reversal

Optimism also remains intact on the stock market and analysts see further upside potential: the average 12-month price target is CHF 184.30, around a tenth above the current level. The most optimistic estimate even reaches CHF 220, which corresponds to a potential increase of around 30 percent.

Against this backdrop, the recent price decline looks less like a warning signal and more like a pause for breath after a strong run. Fundamental doubts are hardly recognizable. On the contrary: Sulzer is demonstrating operational discipline, rising margins and strategic clarity. For trading-oriented investors, the current setback could therefore be more of a buying opportunity.

Investment solutions

Investors who want to bet on a turnaround towards a high can lie in wait in the currently volatile market and invest in the Long Mini Future ISU1LZ from ZKB to bet on this scenario. The leverage product offers a multiplier of 5.7 and thus benefits disproportionately from rising prices of the underlying. The knock-out is located at CHF 138.3161, 13.8% away from the current price level. The mini future offers a little more leeway on the downside, and therefore a lower risk MSUBET from Leonteq. The stop-loss level is at CHF 114.92, which in turn means a distance of 28.4%. However, the higher buffer comes at the expense of leverage, which is “only” 3.2.

Anyone assuming that the breather in the Sulzer share will last a while longer can buy the Barrier Reverse Convertible SBMZJB from Julius Baer with a remaining term until July 2027. The product offers the prospect of a return of 19.6% p.a., with a barrier at CHF 122.10 – a solid buffer of 23.8%.