The final instance

-

Wolfgang Hagl

Redaktor

Precious metals should not be missing from a diversified portfolio. There are many arguments in favor of this thesis. In my view, the most important one is that gold is and remains the only real substitute currency.

I had my first conscious encounter with gold in 1984, when as a 10-year-old I was enthralled by the Summer Olympics in Los Angeles. I was one of the more than 2 billion people who watched the opening ceremony on television. The flight of the rocket man through the Memorial Coliseum, which was packed with almost 100,000 spectators, is just as memorable to me as the triumphant performances of Carl Lewis later on. With 4 gold medals, the US sprinter and long jumper became a superstar. In sport, gold has more of a symbolic meaning – the trophy from the Los Angeles Games, for example, is made of gold-plated silver. For me, however, there is no more fitting and beautiful award than the shiny medal.

A firm conviction

The memories of the 1980s may have contributed to the fact that gold still accompanies me today in my profession as a financial journalist. I particularly enjoy writing about the precious metal. This work has led to the conviction that gold should be as much a part of a diversified portfolio as a medal at the Olympics. I share this opinion with many others. People have been using gold as a means of payment for thousands of years. In modern times, the precious metal has increasingly mutated into a substitute and crisis currency.

This character is only possible because there is only a limited amount of gold. According to figures from the World Gold Council (WGC), a total of around 216,000 tons of the yellow metal will have been mined by the end of 2024. Compressed, this quantity corresponds to a cube with an edge length of just 22 meters. Nevertheless, there can be no talk of an acute shortage. In the period from 2015 to 2024, the gold supply averaged just under 4,800 tons per year. Three quarters of this quantity came from mining, the rest from recycling. At 4,338 tons, annual demand fell well short of supply during this decade.

Amazingly low allocation

Nevertheless, the price of gold has more than doubled in the period under review. The short-term surplus therefore does not diminish the appeal of the precious metal. And for good reason: even a marginal change on the buyer side could push the market balance into deficit. New mining projects require a lot of capital and have a long lead time. On the gold market, therefore, a relatively inelastic supply meets steadily growing interest on the part of investors. The share of the precious metal in global capital allocation is still surprisingly low. In 2022, private investors held gold worth just under USD 3 trillion, which corresponded to only 1% of their total financial assets (bonds, equities, alternative investments and gold).

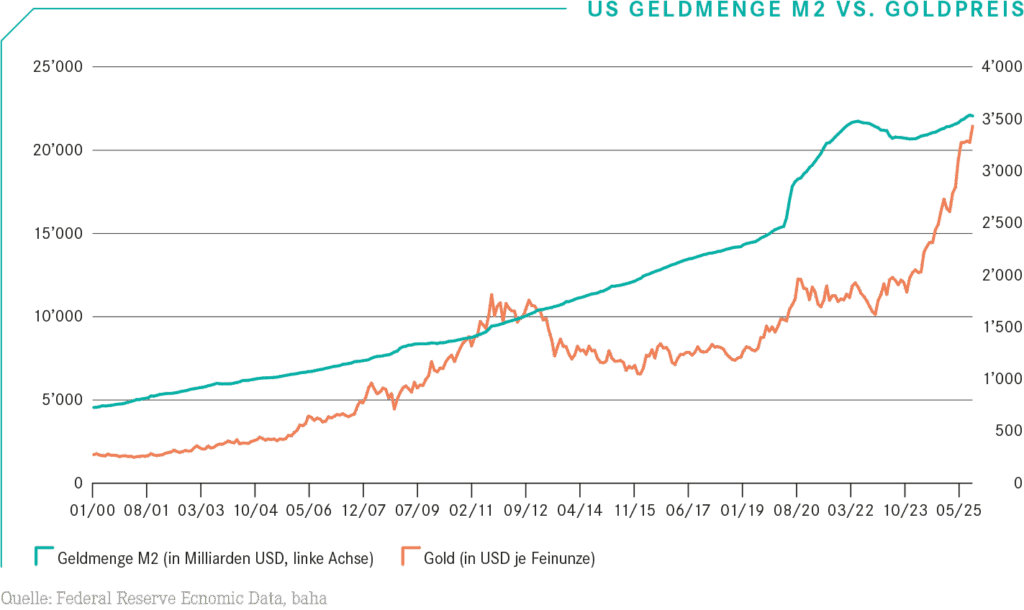

However, it will not stay that way. The massive expansion of traditional (paper) money systems in particular suggests a rising rate. One example is the USA: at the end of August 2025, more than USD 22,000 billion was in circulation. Since the turn of the millennium, the M2 money supply has thus increased almost fivefold. With “fresh money”, the states have survived various crises. These included the bursting of the dotcom bubble in 2001, the real estate crisis of 2008/2009 and, most recently, the coronavirus pandemic. For a long time, this seemed to make little difference to the status of the US dollar as the global reserve currency. In addition to the sheer strength of the world’s largest economy and the government’s ability to service a growing debt burden, it was above all the Federal Reserve System’s achievement in maintaining this status with a balanced monetary policy.

Fed under fire

But now the independence of the US Federal Reserve is more at risk than ever before. President Donald Trump has been attacking its head Jerome Powell for months. Although inflation in the US remains stubbornly high, Trump is calling for interest rate cuts and is not afraid of personal insults or the dismissal of a high-ranking Fed member.

It is therefore not surprising that gold is experiencing an unprecedented surge in the year of the Republicans’ return to the White House. At the end of September, the annual balance sheet showed an increase in value of more than 40%. If the troy ounce can maintain this gain, it will have its best year since the late 1970s. The persistently high interest rate level of the US dollar is clearly not deterring investors from turning to the crisis currency. Most recently, the 10-year US government bond yielded around 4.10%. As gold itself does not generate any current income, USD interest rates are seen as an opportunity cost of owning the precious metal.

Taking inflation into account, the situation is of course somewhat different. The 10-year USD real interest rate was just under 1.60% at the end of September. It looks as if opportunity costs will continue to fall, as the Fed cut its key interest rate in September for the first time since 2025. The market is expecting two further monetary easing measures in the US by New Year’s Eve. Regardless of this, Donald Trump is unlikely to stop criticizing the monetary authorities. According to J.P. Morgan, gold is one of the most effective insurances against the central bank’s eroding independence. The major US bank has just revised its price forecast upwards. The precious metal could reach the USD 4,000 per troy ounce mark by the beginning of 2026.

Spectacular hypothesis

J.P. Morgan published an interesting study back in May. In it, the analysts hypothesized that gold could rise to USD 6,000. To achieve this, it would be sufficient for foreign investors to shift just 0.5% of their USD-denominated investments into the precious metal. The figures presented are interesting: since 2017, inflows of around USD 26 billion per quarter have been enough to keep the gold price stable. With an additional USD 10 billion, investors and central banks were able to trigger a price increase of 3% compared to the previous quarter. In fact, the first three months of 2024 saw an average demand for gold of USD 52 billion per quarter.

Of course, this trend could come to an end, for example if the political situation in the US calms down or inflation falls sharply. Nevertheless, I can still see a lot to be gained from the analysts’ theses and I remain convinced that gold is a “last resort” within the asset classes. In my view, the meteoric rise of cryptocurrencies, above all Bitcoin, does nothing to change this. For me, gold is the last resort where everything comes together in times of crisis and inflation. And as much as I would like to see a more peaceful world, it is hard to imagine my generation experiencing another phase of harmonious and low-conflict geopolitics. However, this does not change the fact that gold will continue to go through phases of weakness in the future. Structurally, however, the trend is clearly upwards.

In less than three years, the Olympic family will return to California. The opening ceremony will take place on July 14, 2028 at the LA Memorial Coliseum. I will probably spend many hours in front of the TV again to admire the athletes and their shiny medals. However, the organizers have not yet revealed what the design of the medals will look like. In any case, gold will shine more than ever. I can well imagine that a troy ounce will cost more than USD 5,000 in the summer of 2028.

Investment Solution

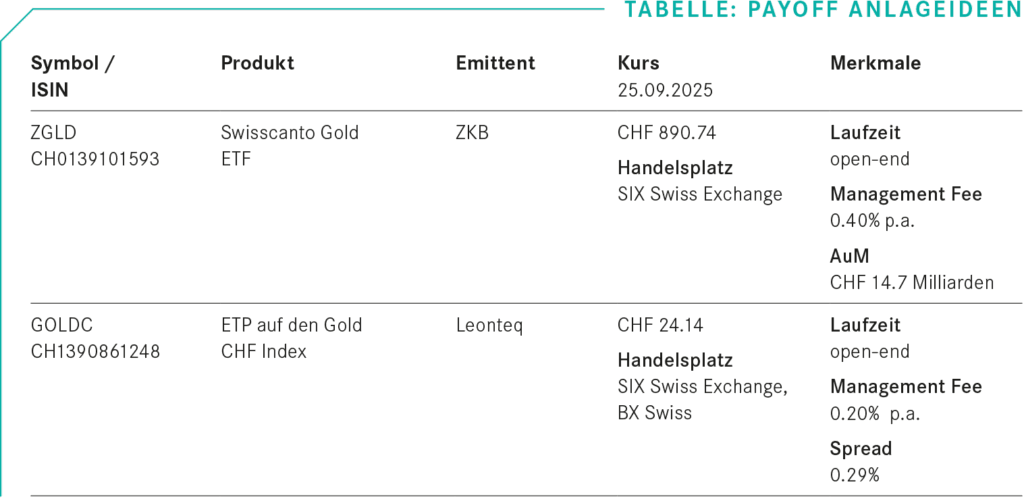

There are various ways to include gold in your portfolio. When buying coins or bars directly, secure storage, for example in a bank safe deposit box or in your own vault, must be taken into account. Physically backed investment products are a cost-effective alternative. One of the largest vehicles of this type is the Swisscanto Gold ETF ZGLD. March 2026 marks the 20th anniversary of the launch of this exchange-traded fund. ZKB currently manages around CHF 14.7 billion in seven different currency classes. This brings the total amount of gold stored by the cantonal bank to around 155 tons. Investors can have their shares delivered in the form of standard bars weighing around 12.5 kilograms. However, this requires a substantial investment, as this quantity is currently valued at around CHF 1.16 million. An ETF costs around CHF 890 and secures the investor 9,237 grams of the metal.

Leonteq has packed gold into the passive investment in a significantly smaller denomination. Last fall, the Zurich-based fintech launched the ETP GOLDC was issued. The structured product tracks the crisis currency via a special index. Fluctuations between the commodity currency USD and CHF are excluded on a daily basis. The ETP is not collateralized with real gold and – unlike the ETF – is not a protected investment fund within the meaning of the CISA. However, Leonteq deposits a pledge with SIX SIS Ltd for each product. SIX Repo Ltd is responsible for the ongoing valuation and monitoring of the collateral and thus represents the investors. In the event that Leonteq gets into payment difficulties (default), SIX Repo Ltd could realize the pledge in favor of the product holders.